EMAIL NEWSLETTER JUNE

2005

Welcome

again to the McLean

and Co. Newsletter

in which we discuss current taxation and business matters. We trust

you find it informative. Any feedback would be welcomed.

McLean

and Co. is a

home based chartered accountancy practice based in Clive, Hawkes

Bay.

Readers are invited to peruse the practice website

www.mcleanandco.co.nz,

which lists

services

provided, gives contact details and indicates how to become a client, contains

an extensive base of articles on business and taxation matters, and has

links to other websites that may assist your business. Being a

small firm itself, McLean and Co. strives to provide a personal and

professional service largely to a self employed person and small business client

base. Enquiries are welcomed.

We

are happy to accept new clients. Please contact ourselves at the contact

points highlighted above if we can assist you in your accounting and taxation

requirements. Our website lists information required for this in the following

link:

INDEX

-

Who

Pays Tax.......and How Much?

-

Individual

Income Tax- Common Questions

-

Franchise Section on our Website

-

Latest

Credit Card Data

-

Contractor

or Employee?

-

How

to Increase your Investment Returns through Gearing

RELEVANT

BUSINESS AND TAXATION ARTICLES

The

McLean and Co. website contains an extensive number of articles prepared by

McLean and Co. relating to taxation and business matters. Here

are a selection that will be of interest:

WHO

PAYS TAX........AND HOW MUCH?

The following were some key finanancial facts detailed in the

2005 Budget

| Individual taxable income |

Number of people

|

Tax paid

|

|

($)

|

(000) |

% |

($m) |

% |

|

Zero

|

178

|

6% |

0 |

0% |

|

1-10,000

|

495

|

16% |

311 |

1% |

|

10-20,000

|

994

|

32% |

2,471 |

12% |

|

20-30,000

|

360

|

12% |

1,674 |

8% |

|

30-40,000

|

309

|

10% |

2,135 |

10% |

|

40-50,000

|

253

|

8% |

2,448 |

12% |

|

50-60,000

|

141

|

5% |

1,824 |

9% |

|

60-70,000

|

104

|

3% |

1,725 |

8% |

|

70-100,000

|

141

|

5% |

3,251 |

15% |

|

100,000+

|

85

|

3% |

5,295 |

25% |

|

All

|

3,060

|

100% |

21,134 |

100% |

This table includes tax on New Zealand Superannuation and major Social

Welfare benefits, but excludes ACC levies and anyone who is under 15.

Data are projected for the year ended June 2006.

|

AVERAGE INCOMES

| Average individual wage earnings: |

($)

|

| - full-time earner |

42,920 |

| - part-time earner full year |

15,878 |

Full-time earner works for more than 30 hours per week.

|

| Average family gross income: |

($) |

| - couple with children |

82,370 |

| - couple with no children |

67,829 |

| - sole parent |

26,324 |

| - single person |

26,720 |

Includes benefits and other non-wage income for year ended

June 2006.

|

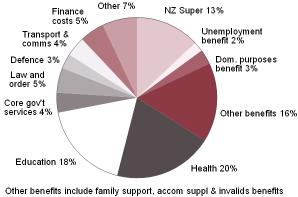

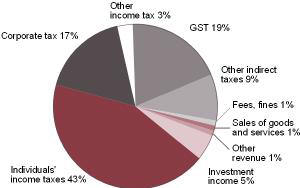

Core Crown Expenses in 2005/06

$48.2 billion

Core Crown Revenue in 2005/06

$53.3 billion

INDIVIDUAL

INCOME TAX- COMMON QUESTIONS

How do I get a record of what salary or wages I

received for the year?

You can request a summary of earnings from Inland Revenue Department.. This

shows your income paid and tax deducted by each employer and ACC earners' levy

paid.

In previous years I have included the cost of my

income protection insurance. Can I still claim this?

Expenses such as income protection insurance can be offset against your

taxable income. This reduces your taxable income by the amount of your

expenses, and therefore reduces your tax.

Depending on your circumstances, you can claim expenses in one of the

following two ways.

| You can claim expenses on a personal tax summary. You may receive one

automatically in June from Inland Revenue department but if not, phone IRD in July to ask for one. You can

either:

| Tell IRD about the expenses over the phone, or

| Fill in your expenses and send the personal tax summary back to

IRD. |

|

| If you file your IR3 tax return, you can claim your expenses at Box 25. |

|

What are some of the expenses I can claim if I am a

salary or wage earner?

Expenses you claim are:

| commission on interest or dividend income (but not bank fees, as they

are private expenses)

| interest on money you borrowed to buy shares or to invest - as long as

the investment will produce taxable income

| premiums for loss of earnings insurance, provided the benefit from the

insurance policy is taxable income

| expenses incurred in earning income that has had withholding tax

deducted

| additional expenses incurred in earning partnership income, such as

interest on capital borrowed to purchase a share in the partnership

| fees you paid someone to complete your tax return. |

| | | | |

These last three expenses are usually claimed on an IR3 tax return as they

are business expenses and not associated with salary and wage earners.

Is it compulsory to be on the right tax code?

Yes, this is covered in section NC 8 of the Income Tax Act 2004.

What happens if I don't give my IRD number to my

bank or employer?

Your IRD number is the link between Inland Revenue Department and your bank or

employer. If you don't provide your IRD number to your bank or employer they

are required to deduct tax at the no-declaration rate. This is presently 45%

on salaries and wages, and 39% on interest.

Why isn't a personal tax summary issued

automatically to everyone?

Most people pay the correct amount of tax during the year, so they don't

need to deal with IRDs at the end of the year.

If you aren't sent a personal tax summary and you don't have to request

one, you can choose to request one after July.

Why can't I claim rebates for a housekeeper,

childcare or donations on my IR 3?

The rebate claims process is now separate from the tax return process. This

means you can get your rebate earlier - you won't have to wait until your IR 3

return is filed and processed. You'll get a rebate claim form (IR526)

automatically in April if you've claimed a rebate in the past, if you do not

receive one you can download one from www.ird.govt.nz

or request one from Inland Revenue Department. Complete it , sign it and post it in with

your receipts.

Why is the personal tax summary not available until

July when I used to get my taxpack in April?

Personal tax summaries can't be issued until all the employment details for

the year have been processed. Employers don't have to file the final month's

details (for the March month) for the tax year until 20 April, after which we

can process the information and generate the personal tax summaries.

How much tax will I pay if I have been made

redundant?

The tax you pay will depend on the combined total of the redundancy payment

and the grossed-up annual value of your income for the previous four weeks.

| If the total is $38,000 or less, you will be taxed at 21%.

| If the total is between $38,001 and $60,000 inclusive, you will be taxed

at 33%.

| If the total is over $60,000, you will be taxed at 39%. |

| |

Redundancy payments are not liable to earners' levy.

FRANCHISE

SECTION ON OUR WEBSITE

We have introduced a Franchise Section to our Website. The

following are the articles in it:

A

Consumers Guide to Buying a Franchise

Franchising

Basics

Franchising- Advantages/

Disadvantages

Pros

and Cons of Starting a Franchise

Buying

a Franchise- What you should Consider

Finding

the Perfect Franchise Opportunity

The

Franchise Agreement

Evaluating

a Franchise Agreement

Fifteen

Questions to Ask before Choosing a Franchise

Typical

Franchise Fees

Eight Steps

to Starting A Business

Looking at

Buying a Business- How Do I Decide which is the Right One?

Creating a

Successful Market Niche

Business

Strategy- a Choice of Three

Starting

in Business- Basic Tax Obligations

Business

Legal Structures

Comparison between Sole

Trader, Partnership and Company

Sole Trader

Business Structure- Advantages/ Disadvantages

Partnership

Business Structure- Advantages/ Disadvantages

Company

Business Structure- Advantages/ Disadvantages

Buying

a Business- Advantages/ Disadvantages/ What to Look for

Obtaining

a Business Loan- Key Steps

Borrowing

Money

What

you Need to Know about Record Keeping

LATEST CREDIT

CARD DATA

The latest credit card statistics show that:

| At the end of April we owed $4.076 billion dollars on our credit cards,

net of deposit balances

| Our billings totalled $1.8 billion in April, and for the year to the end

of April this came to $22.2 billion

| We used our credit cards overseas to rack up spending of $2.6 billion

over the year to the end of April

| Over the year to the end of March we were charged $503 million in

interest.

| The weighted-average interest rate charged in March was 18.8%

| 69.4% of the average amount owed at any time during March was interest

-bearing

|

| | | | |

CONTRACTOR OR

EMPLOYEE?

It is important to know

whether you are employing a contractor or an employee because

the tax, ACC and employment obligations are treated

differently for these two groups of people.

Other terms for a contractor are self-employed, and

self-employed contractor.

The Contractor Catch

Many businesses make the mistake of thinking they can

employ someone as a contractor, when in fact the relationship

is one of employer and employee. In most cases it will be

quite clear whether or not someone is an employee. Generally,

if the employer controls how and when the person’s work is

done, then the person is an employee.

Contractor or Employee?

How does an employer know if a person will be regarded as a

contractor or an employee? Contractors are people who are

employed under a contract for service whereas employees

are employed under a contract of service which requires

employees to be continuously available for the employer and to

accept a high degree of control by the employer.

There are tests you can apply. Two main issues are:

| The degree of control the employer has over the

person and the work involved. How much room for initiative

does the person really have?

| The degree of integration into the business. Does

the employer provide all the resources for the person?

What does the person have at risk? Does the person work

for other businesses as well? |

|

Inland Revenue and the Department of Labour both provide

questions to help define if the person is a contractor or

employee:

Generally, a person who is defined as an employee under

employment law will also be an employee for tax purposes.

1. TAX ISSUES (INLAND REVENUE)

It’s illegal to treat someone as a contractor to avoid

deducting tax. This is because employers are responsible for

their employee’s tax deductions. These include PAYE,

student loans and ACC payments. If Inland Revenue determines

that the contractor is really an employee, then the business

can be prosecuted for failing to deduct tax. In addition,

the taxes themselves will have to be paid.

This makes it important to be clear that the person

you’re employing as a contractor really is a genuine

contractor.

Withholding Tax

Even if the person is a contractor, employers in many

industry categories (such as caretaking, agricultural

workers, milk delivery, modelling and entertaining), are

still required to deduct withholding tax.

To find out if you need to deduct withholding tax check

the categories listed on page 4 of the Tax

code declaration (IR330, PDF 138kb). If in any

doubt, check with the Inland Revenue by calling 0800 377

772.

You’ll find information on how to deduct withholding

tax on page 12 of Inland Revenue’s Employer’s

guide – information to help fulfil your responsibilities

as an employer (IR335, PDF 447kb).

2. EMPLOYMENT ISSUES (DEPARTMENT OF LABOUR)

The key point here is that a business cannot treat an

employee in the same way that it might be able to deal with

a contractor.

Employees have rights under the Employment Relations Act

2000 and other employment laws. Contractors are not covered

by the Employment Relations Act or some of the other

employment laws, such as the Holidays Act 2003. The general

civil law determines most of the rights and obligations of

contractors. Health and safety law applies to both employees

and contractors, although the expectations in each case are

different.

Case Study

A construction company terminated the contract of one of

its contractors for inappropriate behaviour. The person then

brought an unjustified dismissal claim against the company,

claiming that he was essentially an employee. In its ruling,

the Employment Relations Authority conceded that the ‘true

intention’ of the parties was to establish a contractor

relationship, but by applying other tests ruled that in

reality the relationship was one of employer and employee.

The Authority consequently ruled that the person was

unjustifiably dismissed and awarded him lost wages, holiday

pay, and $1,000 compensation for humiliation and distress.

Implications

This case highlights the need for employers to establish

as clearly as possible the real nature of their relationship

with contractors. If the contractor is really an employee,

then the employer cannot simply dismiss the person. Instead

the relationship between the employer and the

‘subcontractor’ must abide by all the provisions of the Employment

Relations Act 2000 and its amendments.

Further information

Inland Revenue

| Get help on the phone from the General Business Tax

Enquiries service on 0800 377 774 (have your IRD number

ready, however a general enquiry does not require an IRD

number). View other Inland Revenue contact

details .

| Arrange

online for an Inland Revenue business advisor to

visit you. |

|

Department of Labour - Employment

Relations

HOW TO

INCREASE YOUR INVESTMENT RETURNS THROUGH GEARING

When buying a rental

property, taking out a mortgage to allow you to purchase it is a common

practice. While a mortgage is usually a means to allow us to purchase a

property we cannot afford to purchase outright, when the numbers are right

gearing allows you to earn a higher return on your initial investment.

In its simplest form, gearing means borrowing to finance income-generating

activities. While the most familiar form of gearing is the probably the

mortgage, other financial instruments such as futures can also be used.

So if you can gear for property investment, can you gear for other

investments as well and reap the benefits? Theoretically the answer is

yes, however not many people to do it. The practicalities (and expenses)

of taking out a loan to buy shares or other investments tend to dissuade

people from considering gearing as an option to help them build their

investment assets and increase investment returns. However, there are

managed funds that use gearing so they can take away some of the hassle.

Gearing is profitable when the cost of borrowing is lower than the return

you earn on your investment. Take, for instance, a person with $200,000 to

invest who plans to buy a rental property (or any other investment) with a

yield of 8.5%. They can purchase a $200,000 house or borrow a further

$200,000 at 7.5% and buy a $400,000 house. The table below shows the

variation in returns that would be earned. This doesn’t necessarily just

apply to property, it could be any other investment too, such as a

portfolio of shares.

As borrowing to invest on your own may seem daunting, you may find that

another option that could enhance your returns is to seek out a managed

fund with a mandate that allows the fund to gear when there are suitable

opportunities. Typically these are growth-oriented funds such as NZ

Equities funds, as there is a cost to borrow that means that you need to

be investing in assets that have the potential to generate higher returns

to cover the cost of borrowing.

Generally there will be limits on the allowable level of gearing (for

instance, the manager may be allowed to borrow up to 20% or 30% of the

funds assets), and even then the manager might not practice it. A

financial adviser should be able to provide you with information on funds

that allow gearing as part of their investment strategy.

Gearing your investments increases risk. With gearing, the risk is that

your returns will not be high enough to cover the costs of borrowing, and

your returns will typically be more volatile. However, as we all know

higher returns must come with higher risks. Using a managed fund that

utilises gearing means that professional investment managers are

constantly assessing whether the environment is right for this approach

and whether the opportunities available justify the risks and costs at any

point in time.

You probably consider borrowing to buy a rental property quite normal,

necessary even, so if you are looking to enhance investment returns then

this could be a strategy for you. As always, we recommend you seek advice

from a financial adviser before deciding on or changing your investment

strategy.

The information

provided in this email newsletter is for informational purposes only.

McLean and Co. accept no responsibility for the opinions and information

expressed in the information provided and it is provided "as

is" without warranty of any kind. The user

assumes the entire risk as to the accuracy and use of this document.

Readers are asked to seek professional advice pertaining to their

own circumstances. The McLean and Co. email newsletter

may be copied and distributed subject to the following conditions:

|

All text must

be copied without modification and all pages must be included.

|

This document

must not be distributed for profit.

|

|